Location, location, location strikes again

Where you buy your home matters far more than what you buy, but not everyone can afford to buy in the right place

I once heard a story that newly employed professors at NYU were given very favorable rental contracts back in the 1970s. This, apparently, proved to be a very bad deal for them, as the favorable rental contracts meant they did not buy housing in midtown Manhattan and thus had to continue working as professors instead of retiring early as real estate investors. As someone who has watched from abroad as Stockholm real estate prices have exploded there over the last 15 years, I have a certain amount of understanding for someone watching real estate prices and thinking, what if I also owned some real estate there? Wouldn’t that be nice?

Because the kinds of house price increases we have seen in major cities around the world will lead to very large increases in wealth for people who own real estate there. Part of the reason is that, for most households, the home they own is their most important asset. Housing typically accounts for more than half of middle-class families' total gross wealth, with the rest consisting mostly of pension wealth.

Now, house prices don’t just change for no reason, and areas with high house price growth also tend to be where wages are rising. In turn, wage increases have tended to occur in areas where income and house prices are already high, such as the central parts of Stockholm, New York, Copenhagen, and London. Not everyone can buy in these areas, because high prices and limited supply just make it too expensive. An alternative story is that some households may not want to live in the big city. In either case, not buying in high-growth areas means that some households are shut out from both large wage increases and high capital gains on their largest asset.

In a new paper with Natalia Khorunzhina and Walter D’Lima, we basically tell this story. Being an academic paper, it of course takes much longer to get to the point. But I think it is an important and interesting story to tell, with implications for how we think about wealth inequality, why financial returns differ across individuals, and the spatial roots of inequality. This post will describe our new paper, which you can read in total here.

The income gradient in housing capital gains

We set out to answer a simple question: do high-income households earn higher capital gains on their homes? And if so, why? The short answer is that they do, and that it’s almost entirely about being able to buy in locations with high levels of house price growth, like Stockholm, Copenhagen, London or New York.

Using administrative data covering every housing transaction in Denmark from 1996 to 2022, we can track exactly what people pay for their homes and what they sell them for. This lets us compute actual, realized capital gains for all buyers.

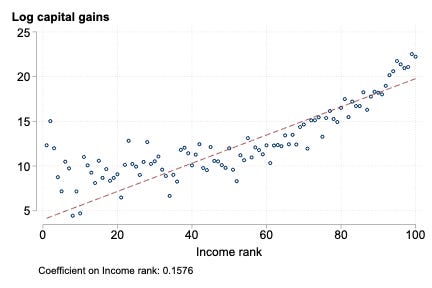

Our first result is summarized in the figure: the higher your income rank, the higher the capital gains on your home. We find that buyers at the 90th percentile of the income distribution earn roughly 1.4 percentage points higher annualized capital gains than buyers at the 10th percentile. Over a typical holding period of 10 years, it amounts to a cumulative gap of about 15 percent. Add some leverage, and that suddenly becomes a sizable difference in wealth-building.

It’s not what you buy — it’s where you buy

The natural follow-up question is, what explains this gap?

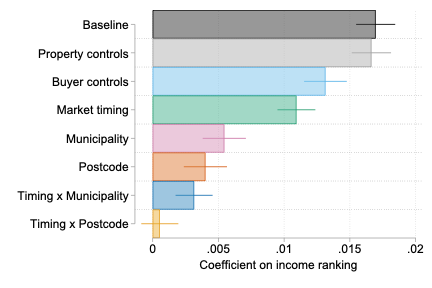

Maybe high-income buyers pick different types of properties (apartments instead of houses, newer buildings, larger homes), which have increased in price. We find this explains almost nothing. Maybe they’re better at timing the market: buying low and selling high. Again, essentially no effect. Maybe higher-income buyers are more educated or wealthier, and are simply savvier investors. Doesn’t look like it.

What then explains the gap? Location. Adding controls for the specific postcode where a home is located eliminates nearly the entire income gradient. Basically, once we account for the timing of purchases and sales within local markets, the coefficient on income rank drops to essentially zero.

This figure is the core result of the paper. Within the same neighborhood and time period, low-income and high-income buyers earn the same capital gains. The implication is that high-income buyers earn higher returns because they buy in areas where prices rise faster.

Why do high-income buyers end up in high-growth locations?

If location is all that matters, why don’t lower-income households simply buy in high-growth areas?

Our answer lies in a fundamental difference between housing and other financial assets. If you want exposure to Apple’s (Novo Nordisk’s?) stock returns, you can buy a single share. Easy-peasy. Housing doesn’t work that way. You can’t buy a fraction of an apartment in Copenhagen. You have to buy the whole thing and be able to finance it. Most buyers in Denmark also live in the property that they own, meaning that they are both consuming housing and investing at the same time. Since we all need a house of a certain size to live in, this puts some constraints on where households can locate: a family of 4 cannot buy a small apartment in Copenhagen just for the capital gain; they instead have to balance capital gains with their housing consumption. I find this to be a very important idea, and one that strongly puts the role of housing consumption and financial constraints at the center of the story of why some people have earned much more than others from their housing purchases.

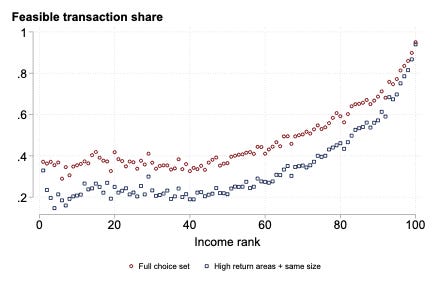

We make an attempt to measure this effect. We construct each buyer’s “feasible choice set” — the share of properties on the market that they could actually afford, given their wealth and borrowing capacity. Buyers in the bottom third of the income distribution could feasibly purchase about 40 percent of available properties. For the top third, it’s over 60 percent. And when we restrict attention to properties in high-growth areas of a comparable size, the gap widens even further. Housing consumption limits the choice set for buyers: not everyone can afford to buy housing in high growth areas, especially if they want to have a certain housing size.

Can mortgage policy fix this?

A natural response might be: well, loosen mortgage rules so that lower-income households can afford to buy in expensive areas. This is a pretty common policy discussion in many countries. Sweden recently changed both the amortization requirement and the downpayment constraint, for example. Trump talked about 50-year mortgages to address housing affordability.

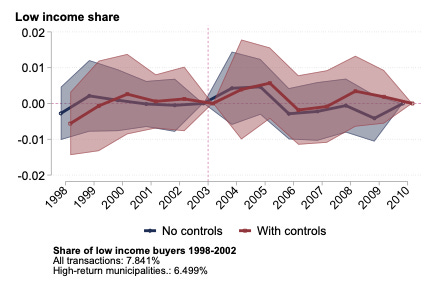

Denmark provides an excellent test case because it went through two major mortgage reforms during our sample period. In 2003, Denmark introduced interest-only mortgages, which substantially reduced monthly payments and expanded borrowing capacity for all households. If credit constraints were the binding barrier, we’d expect to see more low-income buyers entering high-growth municipalities after 2003.

That’s not what happened. House prices in high-growth areas rose sharply, but the income composition of buyers was unchanged. Low-income households gained borrowing capacity, but so did everyone else. One (I think reasonable) interpretation is that in markets with inelastic housing supply, the additional purchasing power was simply absorbed by higher prices.

A similar pattern emerged after 2016, when Danish regulators tightened credit rules specifically for Copenhagen and Aarhus. Despite a policy explicitly aimed at cooling demand in these high-growth cities, the income mix of buyers remained largely unchanged.

The lesson is this: in supply-constrained housing markets, easier credit doesn’t help lower-income households climb the property ladder. It just makes the ladder more expensive.

Final thoughts

What should you take away from all of this? I think the most important thing to remember is that for most households beyond the richest 1 or 5%, differences in the return to wealth mostly reflect differences in the returns to housing wealth. In turn, those differences will mostly reflect where people live.

Where people live will, of course, be partly based on differences in financial resources, but if I want to go a bit beyond the paper, I think we should also acknowledge that not everyone wants to live in cities with high house price growth.

The policy implication is that relaxing mortgage rules is unlikely to expand homeownership access in high-growth areas. Instead, the “solution” probably points toward the supply side. More skyscrapers and easier construction in cities. But that is a topic for another day. Until then!